August Flash Sale — Up To 60% Off

August Flash Sale — Up To 60% Off

Rolling exits allow you to know how much Return or R Multiple you would have made or lost if you had exited your position for a certain amount of time after your original exit.

How does it exactly get calculated?

Let’s go through this example:

Original Trade

- 10:02:00 – Buy 4000 Shares @ 1.2594

- 11:08:00 – Sell 4000 Shares @ 1.4078

Now, let’s assume that instead of exiting at 11:08:00, we exited X minutes later. What would the exit price and return have been?

| Entry Time | Entry Price | Exit Time | Exit Price | Return | |

|---|---|---|---|---|---|

| 10:02:00 | 1.2594 | Original Exit | 11:08:00 | 1.4078 | $593.60 |

| 10:02:00 | 1.2594 | Exiting 1 Min Later | 11:09:00 | 1.4100 | $602.40 |

| 10:02:00 | 1.2594 | Exiting 5 Min Later | 11:13:00 | 1.4150 | $620.40 |

| 10:02:00 | 1.2594 | Exiting 9 Min Later | 11:17:00 | 1.4200 | $638.40 |

| 10:02:00 | 1.2594 | Exiting 1 Hour Later | 12:08:00 | 1.4300 | $676.40 |

From the example above, we can clearly tell that if we had held our position 1 more hour, we would have made significantly greater returns.

Considerations

- Only the last closing execution is considered. We will take the last closing execution quantity and calculate what if this last execution would have been X amount of time later.

How can I use this information to help me make better decisions?

Of course, in hindsight, you can tell that it would have been better to have exited later. However, the true value of this comes into play when you aggregate your data and see the overall picture among all your trades to determine if you are exiting too early.

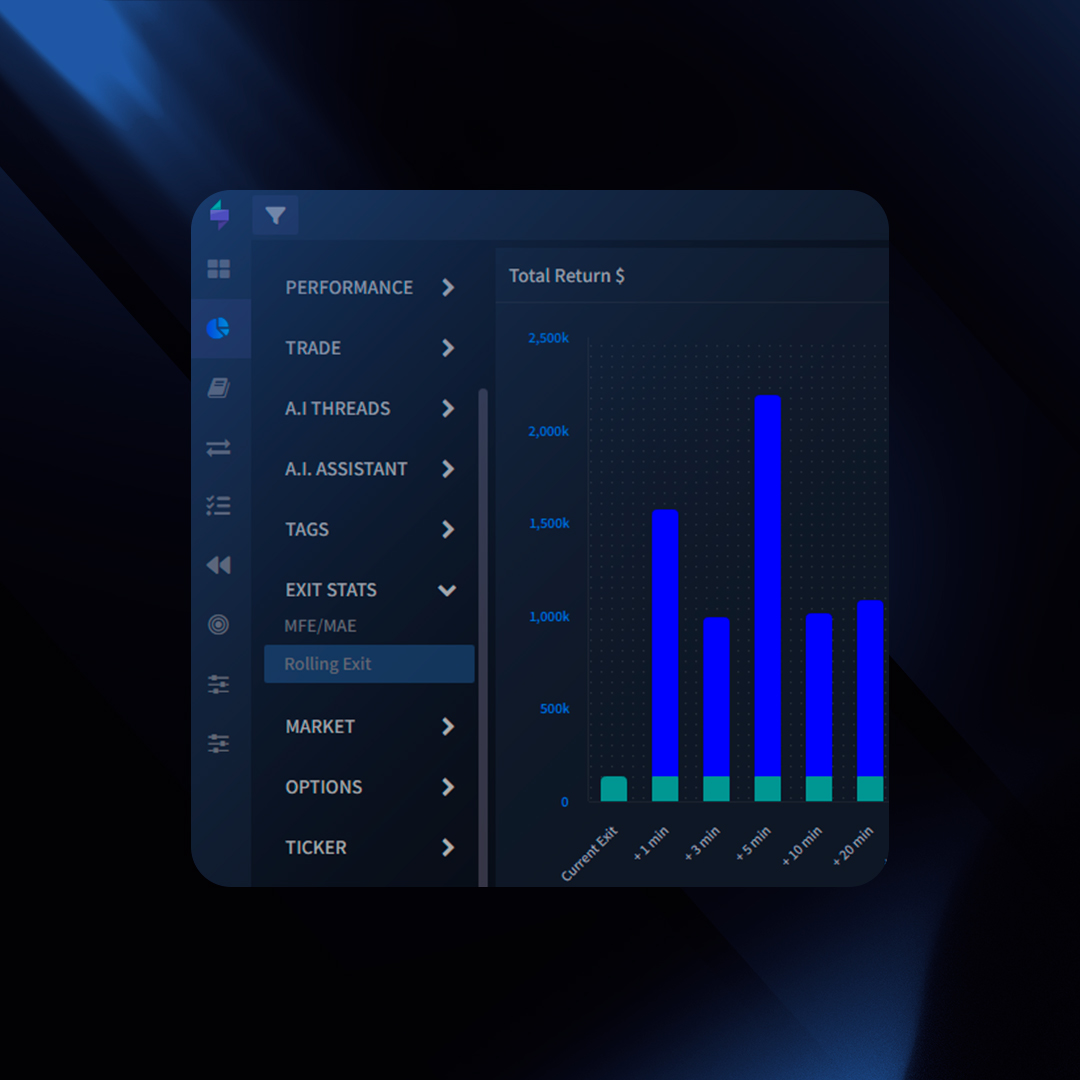

This is something that can be clearly answered in your Rolling Exit report.

The report above shows us what would have been our total extra return if we had moved our last closing execution X amount of time later into the future.

For example, it suggests for this particular example that exiting +10 minutes later could produce an extra $X. This tells us that we might be exiting our positions too early and perhaps we should consider holding them longer for about 10 minutes.

Considerations

- Abnormal results that deviate from your average results will not be considered in these reports as they can provide false positives. For example, if in most of your trades you normally make anywhere from -1R to 2R and there are a few trades with 10R, we will exclude those.

Where to access the Rolling Exit Report?

- Click on “Reports” on the left menu on TraderSync

- On the left sidebar, click the report “Rolling Exit”.